Strong US corporate earnings led by a buoyant tech sector are overshadowing fears that the Middle East conflict could weigh on stocks, according to strategists at Morgan Stanley.

Earnings revisions for the S&P 500 (^GSPC) have moved higher across multiple time horizons over the past month, the team led by Michael Wilson wrote in a note. Second-quarter estimates are up 2% and forecasts for calendar 2026 and the next 12 months have risen 3% and 4%, respectively.

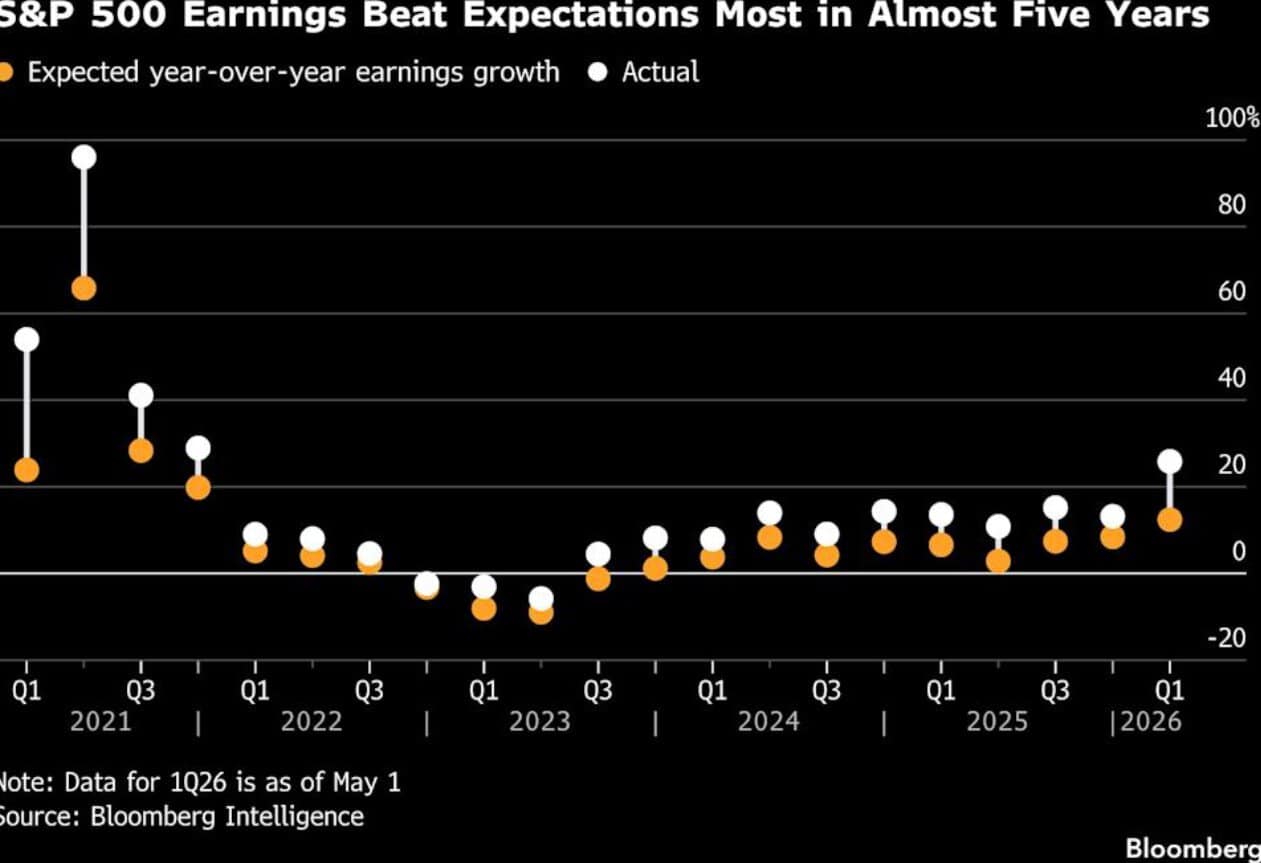

The first-quarter reporting season has delivered robust results, with the median S&P 500 company posting an earnings-per-share upside surprise of 6%. That’s the strongest in four years, the strategists said.

Hyperscalers and semiconductor companies have been been “major contributors to this durability,” Wilson said, as they benefited from accelerating cloud demand and solid order backlogs. “The strength is not limited to these cohorts,” however, as upward revisions have also picked up across financials, industrials and consumer cyclicals, signaling a more durable expansion in profit growth.

The impact of the Iran war is expected to remain uneven rather than systemic, with cost pressures affecting companies on a case-by-case basis rather than weighing on entire sectors, Wilson said. Energy companies, meanwhile, are a tailwind for overall earnings as higher oil prices boost their profit growth.

Despite resilient earnings and US stocks at all-time highs, concentration risks remain a headache for investors, with seven stocks having generated around 80% of S&P 500 returns since the start of the year.

Still, Goldman Sachs Group Inc. strategists led by Ben Snider said the spending boom on AI infrastructure is showing no signs of slowing, with analysts having further ramped up their estimates for hyperscaler spending since the start of earnings season.

“The surge in spending estimates is driving a similar rise in earnings estimates for AI infrastructure companies, helping lift the earnings outlook for the broad market and skewing risks to our S&P 500 EPS estimates to the upside,” Snider and his colleagues wrote.