The stock market has a long history of getting carried away by the future.

Railroads, radios, refrigerators, personal computers, the internet — even ballpoint pens — all helped inflate bubbles around innovations that eventually became part of everyday life.

Now the Nasdaq 100’s (^NDX) AI-fueled surge is starting to look like the next entry in that very strange history.

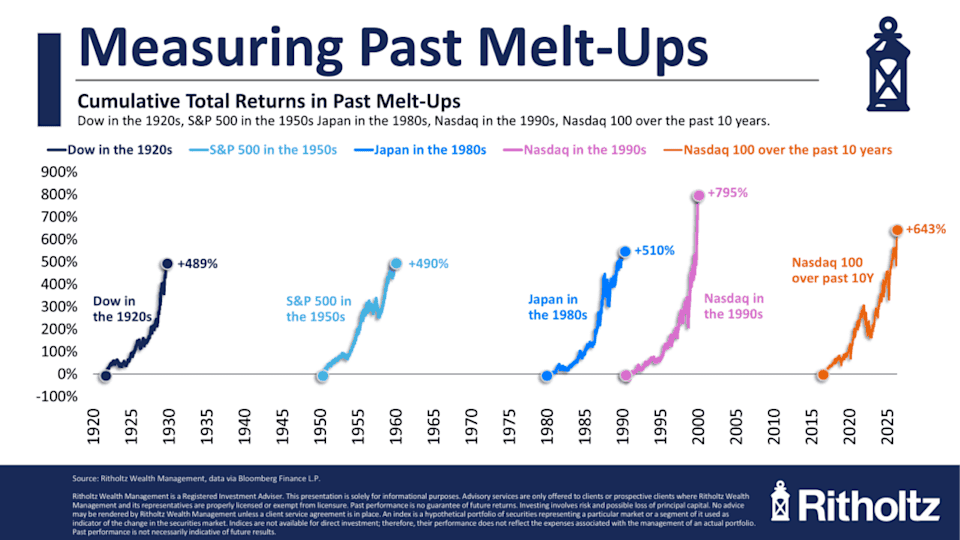

The Nasdaq 100 is no longer simply having a great decade. Its 10-year return of over 640% has now passed some of the most famous booms in market history, including Japan in the 1980s, the Dow (^DJI) in the Roaring ’20s, and the S&P 500’s (^GSPC) postwar surge in the 1950s, according to Ben Carlson of Ritholtz Wealth Management.

Only the 1990s Nasdaq run still sits ahead.

That puts today’s AI trade in rare company — and in a long tradition of investors falling hard for technologies that are real, useful, and almost impossible to value in real time.

A 2018 paper published in Marketing Science studied 51 major innovations from 1825 to 2000 and found bubbles in 37 of them, or roughly 73%. The list reads like a museum of everyday life before it became everyday life: steam engine trains, telegraphs, automobiles, radio, airplanes, television, microwaves, personal computers, mobile phones, the internet, smartphones, and, yes, ballpoint pens.

The weirdness is part of the lesson. Markets have repeatedly overpaid for the future. But the future has often shown up anyway.

The Roaring ’20s were not just flappers, jazz, and margin debt. They were also a technological boom that changed how people lived, traveled, ate, and entertained themselves. The paper found bubbles tied to automobiles, motion pictures, refrigeration, airplanes, and radio, with several peaking around 1928 and 1929.

The 1950s are a different kind of comparison — less mania, more diffusion. Postwar America was scaling households, suburbs, appliances, corporate profits, and consumer demand. The study flags postwar innovation bubbles in products including ballpoint pens, magnetic tape players, microwave ovens, and later, videocassette recorders.

Japan’s 1980s boom sits in a different bucket. That was less about one breakthrough that rewired the economy and more about a marketwide asset bubble wrapped around industrial dominance, easy credit, and the belief that Japan Inc. had cracked the code.

The 1990s Nasdaq boom is the easiest modern comparison because the internet was both a bubble and a civilization-level invention.

The paper found an internet bubble that began in February 1998, peaked in February 2000, and ended in March 2000. It also found that internet-linked parent firms returned over 570% during the bubble period versus about 55% for the broader market.

The mistake in 1999 was not believing in the internet. The mistake was believing every internet stock could become the internet.

AI has a similar tension. The technology can be real, the winners can be enormous, and the trade can still get ahead of itself.

The paper found innovation bubbles tend to form around technologies that are radical, highly visible, and capable of spawning other businesses around them. That is AI’s bull case — and its risk. The more a technology makes other products possible, the harder it becomes to value.

Chips make models possible. Models make software tools possible. Software tools make automation possible. Automation creates new business models. By the time investors price the whole chain, the spreadsheet starts looking like a choose-your-own-adventure book.

History’s weirdest bubbles do not say AI is doomed. They say the market often finds the future before it knows how to price it.