Inflation is cooling.

Consumer spending continues to be at record highs, while consumer confidence has been trending up. And, after almost two years of rate hikes by the U.S. Federal Reserve, investors are expecting at least a few cuts to interest rates this year.

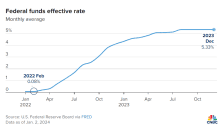

Their anticipation is understandable: The federal funds rate hasn’t been this high since the early 2000s, and some experts say it seems like the Fed has achieved its goal of a “soft landing,” taming inflation without tipping the economy into a recession.

But consumers looking to borrow money shouldn’t start celebrating just yet, said Greg McBride, chief financial analyst at Bankrate.

“Interest rates took the elevator going up; they’re going to take the stairs coming down,” McBride said.

As the Fed goes into its first Federal Open Market Committee meeting of 2024, here’s what that elevator ride up has looked like over the last 12 months in five major consumer categories: credit cards, savings accounts, certificates of deposit, auto loans and mortgages.

Credit cards

Nowhere has that express rate elevator been more obvious than with credit cards. In March 2022, just before the Federal Reserve started its aggressive rate increases, the average annual percentage rate, or APR, for a credit card in the U.S. was 16.34%, according to Bankrate.

Now, almost two years later, that average is 20.74% — almost 4.5 points higher.

Even as the Fed slowed the pace of increases over the last 12 months, the average APR for credit cards rose more than a full percentage point. And it’s jumped almost three-tenths of a point since the last rate hike in July.

![]()

It’s a trend that likely isn’t going to change any time soon, McBride said.

“These prime rates are going to be with us for a while,” he said, so consumers carrying balances on their cards should prioritize and accelerate paying off that debt.

One tool that can really help them do that are balance transfer cards, which allow debt holders to move their balance to a new card that has a lower rate. In some cases, these cards even come with windows of time during which the balance accrues low or no interest.

“Utilize the low rate balance transfer offers that are out there that can shield you from the high rates,” McBride said. “It’s a great tailwind for debt repayment.”

Savings accounts

The bright spot to high interest rates has been for savers, who have finally started seeing bigger rewards for their deposits.

In the last 12 months, the average rate for savings accounts at retail banks has more than doubled, from 0.22% to 0.52%, according to Bankrate.

That average was closer to 0.06% at the beginning of the Fed’s tightening cycle in March 2022.

![]()

But the savviest savers can find rates much higher than that, McBride said.

“The number that savers should be focusing on is actually 10 times higher than that average,” he said. “The top yielding savings accounts are paying well over 5%. Federally insured, available nationwide. You can get to your money when you need it. And many of them are available with no minimum deposit.”

A lot of these are online, high-yield savings accounts that you can open on your smartphone. These accounts can be smart for emergency savings that allow consumers to get their money quickly in a pinch.

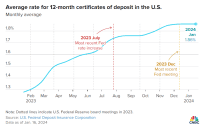

Certificates of deposit

For savers who don’t need quick access to their money and can lock in their deposit for longer periods, the time to get a certificate of deposit is now, McBride said.

The average rate for a 12-month CD has jumped almost six-tenths of a percentage point in the last 12 months, but those rates likely won’t be around for much longer.

“CD yields have peaked,” McBride said. “They’ve already started to ease back, and that’s going to accelerate as the year progresses. So there’s no benefit waiting: You’re not going to get a better yield later.”

Auto loans

Like credit cards, auto loans for both new and used vehicles have also seen noticeable jumps over the last year, rising half a point for both vehicle categories since the Fed’s last rate hike in July.

McBride expects those rates to come down over the course of this year.

“For car buyers, if you’ve got your ducks in a row, the financing environment is going to be better in 2024 than 2023,” he said.

He cautioned, however, that buying a car is still a major expense, regardless of what interest rates are.

“Car payments are budget busters,” he said. “If you don’t have equity from a previous vehicle and you’re buying a $50,000 or $60,000 vehicle, you’ll be financing that amount. So, even if interest rates were still near zero, that’s going to be a backbreaking monthly payment.”

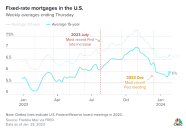

Mortgage rates

Mortgage rates had a bumpy trajectory in 2023, with the average 30-year fixed rate hitting almost 8% in October.

And while they haven’t fallen back to January 2023 levels, the 30-year fixed rate has been hovering between 6.6% and 6.7% for the last four weeks.

McBride expects that cooling trend to continue for the rest of the year.

“As inflation moderates and the Fed begins to trim interest rates, that’s conducive to see mortgage rates trend lower as the year unfolds,” he said. “They will likely be in the sixes most of the year, but we could very easily see mortgage rates move below 6% year-end.”

That may feel like cold comfort to would-be homebuyers who remember when mortgage rates were closer to 3% at the height of the pandemic, but rates closer to 6% will lower monthly payments or let buyers get more house for their money.

“We’re not going back to the 3% of 2021,” McBride said. “But it is a notable improvement from the 8% that we saw in October 2023.”