The world’s largest cryptocurrency exchange, Binance experienced record levels of bitcoin, ethereum and stablecoin withdrawals alongside the implosion of rival exchange FTX.

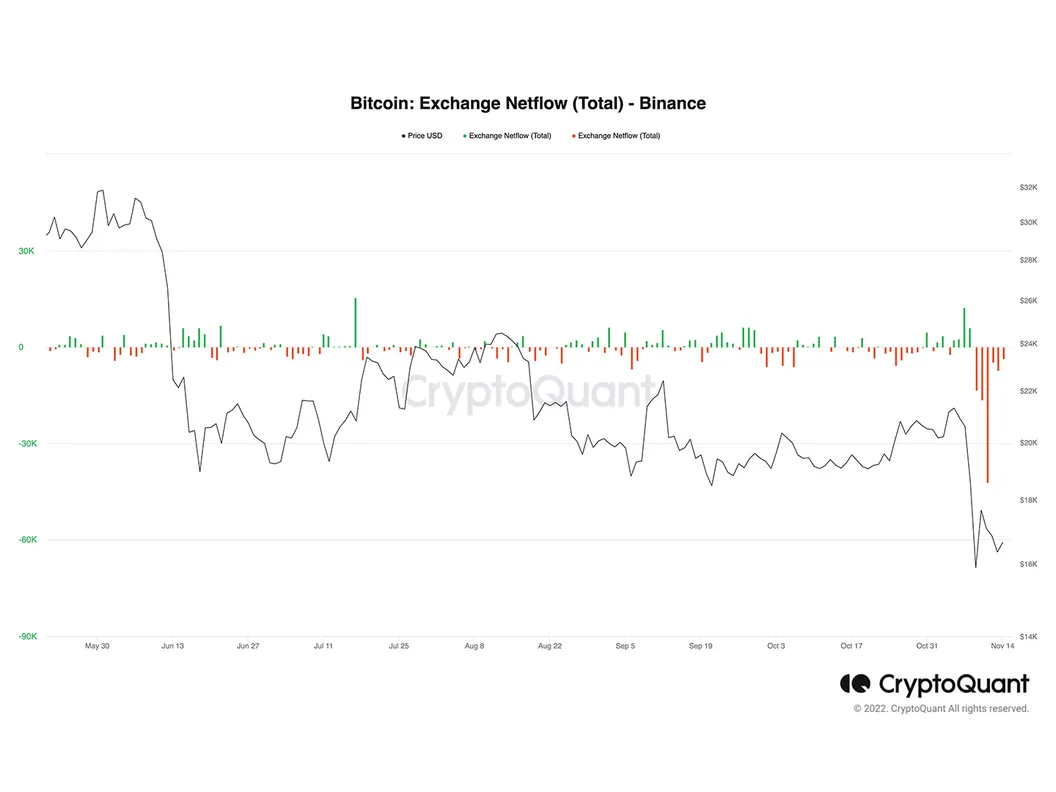

Binance saw a net 81,712 bitcoin ($1.35 billion), or more than 15% of the roughly 500,000 bitcoin on its exchange, pulled from the platform over the past six days, according to data from CryptoQuant. In addition, a net 125,026 ether ($155 million) and $1.14 billion in stablecoins were withdrawn from Binance over the same period.

Appearing on a Twitter space on Monday morning, Binance CEO Changpeng Zhao appealed for calm, and said a “slight” uptick in the pace of withdrawals is normal when the prices of cryptocurrencies drop.

The withdrawals are an industry-wide issue, with Coinglass showing nearly 200,000 bitcoin pulled from exchanges over the past seven days bringing the level of bitcoin held on exchanges down to 1.88 million. Coinbase (COIN), Gemini and Kraken are among the crypto brokers seeing percentage declines similar to Binance.

The fast exits were prompted by the implosion of FTX, which was one of the largest exchanges before it filed for bankruptcy last week. Speculation over the company’s financials mounted following a CoinDesk report that identified holes in the balance sheet of FTX sister company, Alameda Research. Customers scrambled to quickly withdraw funds from FTX, resulting in a liquidity crunch.

Within days, FTX had seen its own bitcoin balance fall from about 20,000 to just one.

Binance made an attempt to acquire FTX at the start of last week, signing a non-binding letter of intent only to walk away from a deal 24-hours later.

Binance did not immediately respond to CoinDesk’s request for comment.