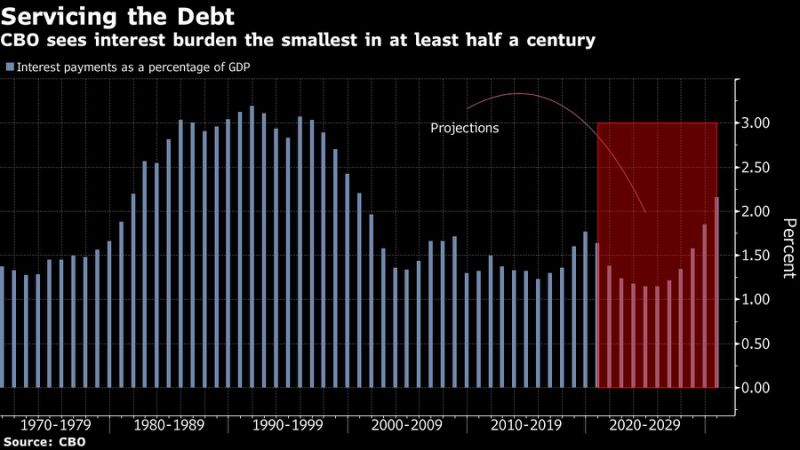

The U.S. government is paying less as it borrows more, one reason investors appear more comfortable than Congress about funding another leg of stimulus.Interest payments in the federal budget declined about 10% in the first 11 months of this fiscal year, when America was running up its biggest deficit since World War II. Over the next few years, servicing the national debt will be cheaper than any time in the past half-century when measured against the size of the economy, according to the Congressional Budget Office.

That’s because yields in the $20 trillion U.S. Treasury market plunged to record lows early in the pandemic — and they’ve risen only slightly since then, even though the supply of debt has surged to a record.Borrowing probably won’t always be this cheap, but for now the U.S. government is far from running up against any financial limits, as it seeks to shore up the economy after a wave of shutdowns and layoffs. Concerns that the country can’t afford much more spending have been voiced by officials from both political parties in recent weeks, as stimulus efforts ground to a halt.

“While there’s been a lot of concern about the mounting debt, it hasn’t caused the problems that were anticipated by the doomsters,” says Ed Yardeni, founder of Yardeni Research Inc. “It’s not just a question of how much debt is outstanding, but what is the cost to service that debt.”

The CBO predicts a deficit of about $3.7 trillion this year, or 16% of GDP, more than triple the year-earlier figures. Bonds issued to fund the shortfall have pushed the U.S. public debt past $20 trillion –- more than the economy’s annual output.

‘Not Stretched’

Yet the average yield on the debt has dropped to 1.7%, from 2.4% in December, and it’s set to fall further.

Even after a few auctions that saw signs of faltering demand, the government can borrow for 30 years at below 1.5%. And the Treasury has tilted sales toward such longer-term securities, helping lock in historically low rates. The latest long-bond auction on Thursday drew a solid bid.

“The U.S.’s debt affordability is quite OK, not stretched by any means,” says Felipe Villarroel, a portfolio manager at TwentyFour Asset Management in London. “We also look at what is the perceived use of the money a government is borrowing, which is now widely accepted as necessary.”The idea that governments need financial-market approval for their budget policies has in any case been called into question.

Anti-Vigilante

Yardeni coined the term “bond vigilantes” in the early 1980s. It described investors who were supposed to exert power over governments by selling their bonds, or merely threatening to, and thus making deficit-spending more expensive.

But now the dominant presence in markets is a kind of anti-vigilante, which does the opposite of all those things: the Federal Reserve.

Fed purchases have siphoned about $1.8 trillion of government debt out of the market since March, while the Treasury was issuing some $3 trillion of new bonds. The central bank is currently adding about $80 billion of Treasuries a month. It’s also promised to keep short-term rates at zero for the foreseeable future and tolerate above-target inflation, while urging the government not to ease up on fiscal stimulus.

Stanley Fischer, former vice chair of the Federal Reserve, said Friday in a Bloomberg Television interview that a low interest-rate burden means the Fed can do more to bolster the economy.

“It means that the Fed can keep going with very cheap money, that it can go on for a much longer time at this rate,” he said.

There’s a broad consensus among bond investors that if rates on longer-term government debt start to creep up, as they’ve occasionally threatened to, then the Fed can and will step in.

‘Still Out There’

“If there were some bond vigilantes still out there to push the bond yields higher,” is how Yardeni puts it, “then the Fed will target the bond yields.”

In an Aug. 31 speech, Fed Vice Chair Richard Clarida left the door open to a policy of capping Treasury yields at some point, though he indicated it’s not imminent.

Even the potential for such a move is helping to keep the government’s borrowing costs down, investors say.The 10-year Treasury note has been trading around 0.7% for weeks, and it’s forecast to end the year within a few basis points of that level, according to Bloomberg surveys.

‘Look Different’

In the financial world there are plenty who argue that the low interest bills America currently pays on its growing debt are just a short-term respite –- like a teaser rate on a jumbo mortgage.

“The Fed is greasing the system to make sure the financial markets are functioning well,” says Gary Pollack, head of fixed-income for private wealth management at Deutsche Bank. “But at some point in time the world will look different, and all of a sudden we are going to be stuck with a huge bill.”That view still carries some weight in Congress too, even if deficit hawks –- Washington’s version of bond vigilantes –- aren’t the force they once were.President Donald Trump’s Republican Party has used its Senate majority to push for scaled-back measures in the next pandemic bill. Democratic presidential candidate Joe Biden has promised more spending if he beats Trump in November’s election, but a senior aide told the Wall Street Journal last month that it’s not clear what America can afford because “the pantry is going to be bare.”

‘Not Worth Anything’

Taking the opposite view is the emerging school of Modern Monetary Theory. It argues that countries like America, which borrow in their own currency, can set the interest rates on their debt as a policy variable –- and don’t really need to sell bonds anyway. The risk is overheating the economy rather than running out of market funds.Also cited by the dovish camp is Japan, which has a national debt about two-and-a-half times bigger than America’s (by comparison with their economies). After more than two decades of low interest rates, its debt-servicing cost is approximately zero.

David Levy, chairman of Jerome Levy Forecasting Center LLC, says that ultimately there are limits to government debt –- but the U.S. is nowhere near hitting them, and has room for more borrowing to pull its economy out of the coronavirus slump.“It would take a long time to get to the type of inflationary scenario where people thought the dollar was not worth anything,” he says. “You can keep this process growing without it breaking down.”