For those looking to buy homes, the most popular way to finance a home purchase is to take out a 30-year mortgage. With mortgage rates having been exceptionally low for years, it’s been possible to get extremely attractive monthly payments even on relatively large mortgage loans, and the 30-year term gives homeowners a long time to get their mortgages paid off.

Yet what’s somewhat surprising is that relatively few people look at an alternative to the 30-year mortgage. A 15-year mortgage requires larger monthly payments, but their interest rates are almost always significantly lower. For instance, right now, a typical 30-year mortgage has an interest rate that’s more than half a percentage point higher than what 15-year mortgages charge.

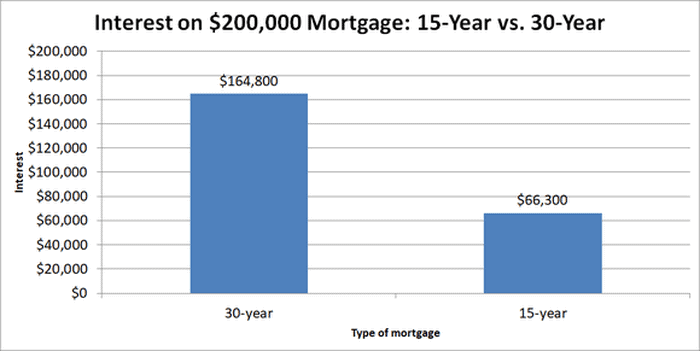

Half a percentage point doesn’t look like a lot. But when you compare the amount of interest you’ll pay on a 15-year mortgage at 4% compared to the corresponding amount on a 30-year mortgage at 4.5%, the difference is astounding.

You actually save twice with a 15-year mortgage. You have a lower rate, but the main reason why you pay so much more interest on a 30-year mortgage is simple: You take twice as long to pay down a 30-year mortgage. For example, on a $200,000 loan, monthly payments on a 30-year mortgage at 4.5% will be around $1,010. A 15-year mortgage at 4% will have monthly payments of about $1,480. The $470-per-month difference pays down the principal balance on the loan that much faster, and over time, that adds up to massive interest savings.

In many real estate markets, prices are too high for many homebuyers to afford a 15-year loan. If you can, however, consider the 15-year option closely. Lower rates and faster payouts will cut the amount of interest that goes to the bank and boost what you keep in your own pocket.