Blue Owl Capital Inc.’s co-chief reeled off all the times he’d seen this type of fear before. Covid. Silicon Valley Bank’s collapse. Liberation Day.

Marc Lipschultz was addressing analysts on the 11th straight day of losses for the firm’s shares, the worst streak since Blue Owl went public almost five years ago. Just weeks earlier, investors yanked more than 15% of net assets from one of the money manager’s tech-focused funds.

But as Lipschultz saw it, this was par for the course when markets get jittery. Some clients in private credit funds like theirs ask for their cash back in times like these. The firm was handling this latest bout of worry just as it had in the past.

It appears different now. Blue Owl last week permanently shut the gates on one of those funds — preventing investors from withdrawing their cash every three months as they’d previously been allowed — and began selling assets to return investor capital.

It’s the latest sign of tumult in a $1.8 trillion market stricken with worry about overspending on artificial intelligence, the technology’s disruptive power and lending standards more broadly. And it’s evoking comparisons to the run-up to the 2008 financial crisis.

“The red flags we are seeing in private credit today are strikingly familiar to those of 2007,” said Orlando Gemes, chief investment officer of Fourier Asset Management. He pointed to worsening lender protections and convoluted liquidity terms that “obscure the mismatch between what investors believe they own and what they can actually exit.”

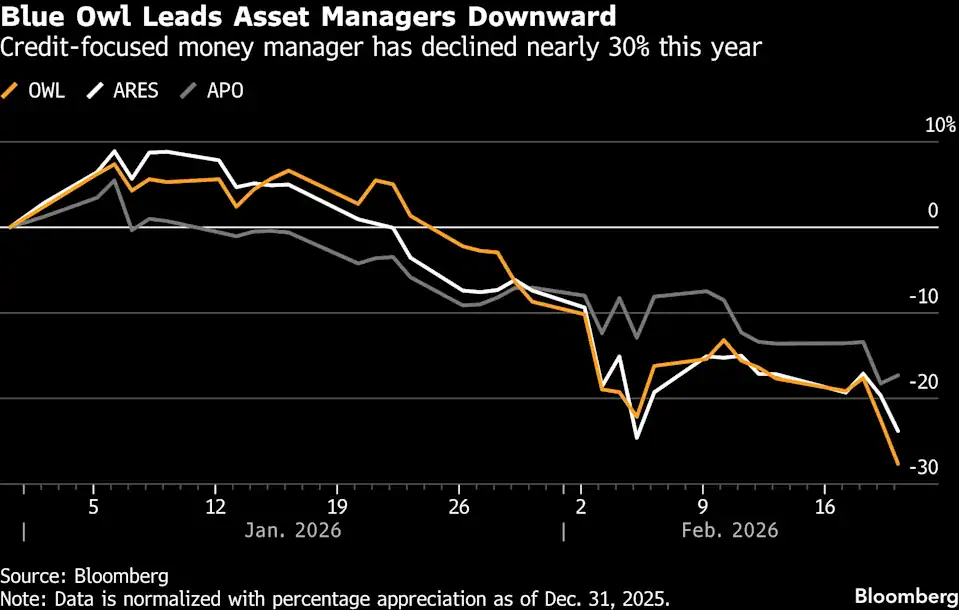

Investors reacted fast. Shares of Blue Owl tumbled as much as 10% on Thursday and triggered a broad decline in the stocks of money managers with fingers in the private credit pie. Ares Management Corp., Blackstone Inc. and Apollo Global Management Inc. were among those dragged down. Blue Owl’s shares have now plunged almost 60% in the past 13 months, even as the firm’s revenue continued to climb in that period.

That a move to limit withdrawals from a $1.6 billion fund drove a $2.4 billion drop in Blue Owl’s market value shows shareholders’ skittishness. Investors in the fund, known as OBDC II, have been gated for months as the firm pursued and then abandoned a plan to merge it with another of its vehicles. Blue Owl is now selling roughly one-third of OBDC II’s loans and handing 30% of investors’ money back to them, a move the firm says is accelerating, not slowing, the overall return of capital. When redemptions were allowed, Blue Owl had the option to limit withdrawals every quarter to 5% of net assets to prevent any forced selling.

“Instead of resuming a five percent a quarter tender, where only tendering investors get a small portion of their capital back, we are returning six times as much capital and returning it to all shareholders over the next 45 days,” the firm said in an emailed statement.

After years of unfettered growth, the once-niche world of private credit has become a linchpin of global finance. Its players are now backing everything from mammoth data center operations to multibillion dollar buyouts of software makers and healthcare companies — far from the industry’s roots funding middling businesses that fell through the cracks of the banking system.

That’s bringing ever-more scrutiny to a market that has always had its naysayers. Despite years of solid returns and remarkably few blowups so far, direct lenders like Blue Owl can’t seem to shake fears about the business model as a whole. Chatter about disparate valuations across lending books stalk executives at every turn. Concerns over the opacity of the market — where debt changes hands infrequently and outside of public view — have dogged the industry for years.

And for Blue Owl in particular, a yearslong streak of acquisitions, aggressive dealmaking and raising funds that cater to individual investors have placed it directly at the center of everything investors worry about most. It’s placing big bets on AI infrastructure that rely on fast growth to make sense. And if AI use does explode, investors fear that the traditional software firms that Blue Owl has lent billions to may be at risk of extinction.

As for investors in OBDC II, those who want fully out will have to wait — or sell at a discount. Hedge funder Boaz Weinstein on Friday offered to buy stakes in OBDC II and other Blue Owl funds, likely at a 20% to 35% haircut.

It all comes at a particularly sensitive time for alternative asset managers, which have been ramping up their efforts to tap into the $14 trillion sitting in US retirement accounts. US Senator Elizabeth Warren, a Massachusetts Democrat, took the opportunity on Thursday to slam the sector.

“A shadowy private credit firm is suddenly blocking investors from withdrawing their money,” Warren, the ranking member of the Senate Banking Committee, said in a statement. She called for more oversight and transparency of the industry. “The Trump Administration needs to wake up. Stop pushing these risky investments into Americans’ retirement accounts.”

Credit Veterans

Blue Owl traces its roots to some of the most swashbuckling corners of finance. Co-founder Doug Ostrover spent years running junk-bond and distressed-debt desks on Wall Street before co-founding GSO Capital Partners, the credit fund that later became the backbone of Blackstone’s credit division. Co-CEO Marc Lipschultz spent more than 20 years at KKR & Co., where he held leadership roles across private equity, private credit and infrastructure investing.

The two teamed up with Craig Packer, a Goldman Sachs Group Inc. veteran, to launch direct lender Owl Rock Capital in 2016 — just as private credit began its explosive growth. In 2021, the firm created what is now Blue Owl by merging with Dyal Capital Partners, a specialist in taking stakes in alternative asset managers.

Since the Dyal merger, the firm has more than tripled its assets under management through a mix of strong fundraising and acquisitions of specialists such as Kuvare Asset Management and real estate lender Prima Capital Advisers. The rapid growth continued last year, with the firm raising more than $1.25 billion for one of the biggest so-called interval funds, which are tailored to individual investors. By the end of 2025, Blue Owl managed more than $300 billion.

Chasing that growth has led Blue Owl into buzzy themes that are now becoming a headache. In 2023, Packer described the firm as “probably the largest lender” to private equity–backed software companies, the very sector now in the crosshairs of investors worried about AI disruption.

“Many private equity firms were buying software companies at very high valuations — not at nine times earnings, but at 20 or even 40 times,” said Antoine Flamarion, co-founder of Paris-based alternative asset manager Tikehau Capital. There are a few big winners in the software business, but finding them is a challenge, he said.

Blue Owl has spearheaded several multibillion-dollar financings for software providers, including RLDatix and Smartsheet. The basic bet is that corporate clients will prefer to stick with entrenched systems rather than suffer the cost of switching.

The rise of AI is quickly putting that to the test. The possibility that bots like Anthropic’s Claude and OpenAI’s ChatGPT will allow companies to cheaply build their own systems has ricocheted through the market, cratering the stock-market values of companies like Atlassian Corp. and Freshworks Inc.

And that’s showing up in investor withdrawals for Blue Owl. Last month, the lender let investors in one of its technology focused-funds cash in about $527 million of shares, or roughly 15% of the fund’s net assets, according to a regulatory filing. Previously, redemptions had been capped at about 5%, in line with the industry standard.

The performance of the fund, known as OTIC, has held strong, and its liquidity remains “substantial,” Blue Owl said. “We have honored all tender requests ever made in OTIC.”

Lipschultz has, in characteristic style, struck a defiant tone. In the earnings call earlier this month, he said performance has been strong and losses minimal. Investors are ignoring facts and acting out of fear, he argued. More recently he’s taken to LinkedIn, boasting about Blue Owl’s ability to pick the companies that will benefit from AI and avoid those that won’t.

Investors need to “distinguish between a very narrow application that, for example, just processes information or does a very simple, narrow function, versus what we focus on and finance — which are these systems of record that organize business processes,” Lipschultz said earlier this month in a CNBC interview. “And they are, in fact, the adopters of AI tools.”

To his credit, initial analyst reactions to last week’s selloff indicated little concern for the overall health of the business. Blue Owl managed to sell the $1.4 billion of loans at close to par, adding “modest positive” sentiment for private credit as a whole, according to Evercore ISI. And while investor redemptions remain an overhang, the sales “validate” Blue Owl’s loan book, a UBS Group AG analyst wrote.

Others were more downbeat. Mohamed El-Erian, former CEO of Pacific Investment Management Co., questioned whether the news was a “canary-in-the-coalmine moment” for private credit, comparing it to the moments before the 2008 financial crisis.

“Bad credit decisions lead to revelations of liquidity mismatches, and that is always dangerous,” said Kentaro Otani, managing director and head of private markets investment firm Siguler Guff Japan. “There could be others like Blue Owl, but if you are a good credit manager and maintain discipline and proper fund size — also proper investor type in the fund — I don’t think this happens.”

The loan sale has also stoked concern that troubles in credit could simply be shifted into less visible corners of private markets. Among the buyers of Blue Owl’s loans was Kuvare, the life insurance and annuities provider that Blue Owl partnered with in 2024 by buying its asset management unit and investing $250 million into the insurer. The loan sale to Kuvare could provide a template for similar maneuvers between private credit lenders and affiliated insurers, analysts at Barclays wrote in a note.

“If similar transactions are repeated frequently, it would deepen the ties between these two parts of the non-bank sector, which could make it more difficult to track the risk,” they wrote.

AI Exposure

Other pockets of risk are easier to see. Blue Owl has led the charge among private capital firms into the AI infrastructure boom, splashing out billions to stake its claim.

The firm bought digital infrastructure fund IPI Partners in early 2025 for $1 billion. The deal brought with it more than $10 billion of fresh assets and control of Stack Infrastructure, a significant data-center operator. More recently, it struck a deal with the Qatar Investment Authority to create a permanent capital platform for digital infrastructure backed by $3 billion of data-center assets.

It also has fought its way into massive data-center financings with the likes of Oracle Corp. and OpenAI. Last year, it entered a deal to help Facebook parent Meta Platforms Inc. develop a stretch of land in rural Louisiana to house Hyperion, set to become the largest of the technology giant’s 29 data centers worldwide. Hyperion involves more than $27 billion of debt on its own.

It all feeds into what McKinsey & Co. estimated is a $5.2 trillion spending need through 2030 to keep up with the demand for AI computing power. But prominent financiers have not been shy about the potential for froth in AI-linked financing. Ray Dalio, founder of Bridgewater Associates, has said AI is in the early stages of a bubble.

The Blue Owl representative said that the firm’s clients “are very interested in carefully constructed investment opportunities that will benefit from the growth in the buildout of AI infrastructure.”

Fallout from Blue Owl’s move to restrict redemptions is still unfolding. Boaz Weinstein, whose Saba Capital Management offered to buy shares in some private-credit funds managed by Blue Owl, said AI disruption fears aren’t going away anytime soon.

“Private credit was once sold as financial nirvana — effortless double-digit returns in a rising market — but that era is quickly ending,” he said in emailed comments. “Even in good times, the market is now breaking down which signals it is in a spot of great vulnerability.”

To be sure, the funds under pressure at Blue Owl make up a relatively small share of the firm’s assets. These so-called business development companies, however, are the most visible piece of the private credit market. They lay out the names of the companies they lend to and their loan valuations, offering the clearest sight into the health of the overall industry for outsiders.

That also makes them more vulnerable to investor stampedes than vehicles designed for long-term capital commitments. They are, in many cases, accessible to more everyday investors than the institutional-grade funds that draw big checks from pensions and sovereign wealth funds.

But as those sources of capital reach their limits, private credit’s most aggressive players will be increasingly forced to reckon with the flightiness of retail investors.

“This is a classic asset-liability mismatch that can only be solved if both asset managers and investors make concessions,” said Mara Dobrescu, a senior principal at Morningstar Inc. “Semiliquid funds should only be used by investors with the financial ability to weather long stretches — years — without needing their money back. This puts an inherent limit on the ‘democratization’ of private assets.”