Stock Markets

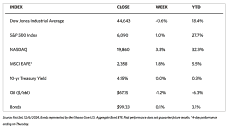

Major stock indexes closed mixed this week. The 30-stock Dow Jones Industrial Average (DJIA) dipped by 0.60%, while the Total Stock Market Index rose by 0.91%. The broad S&P 500 Index climbed by 0.96%, and the technology-heavy Nasdaq Stock Market Composite gained by 3.34%. The NYSE Composite descended by 0.81%. The indicator for investor risk perception, the CBOE Volatility Index (VIX), fell by 5.48%. Sector performance was widely dispersed. Consumer discretionary, communication services, and information technology shares all gained 3% over the week. Energy, utilities, and materials stocks which form the more value-oriented segments of the market all fell over 3%. The geopolitical headlines for the week were dominated by French and South Korean politics, but their impact on U.S. markets was limited.

Other headlines during the week focused on comments from the officials from the Federal Reserve that provided investors with possible clues regarding the pace of interest rate cuts. Federal Reserve Governor Christopher Waller stated that some recent data indicate that progress on inflation may be stalling. Nevertheless, he is inclined to support a cut to the policy rate at the Fed’s upcoming meeting in December if no surprising incoming economic data develops. Fed Chair Powell was more neutral in his comments that “The U.S. economy is in very good shape, and there’s no reason for that not to continue.” Waller’s comments and positive economic news boosted expectations for a 25-basis-point rate cut in December, priced into futures markets.

U.S. Economy

Data released in the past week continued to support a resilient economy and labor market. Both in expansion territory for November were the new orders components of the Institute for Supply Management (ISM) manufacturing and services Purchasing Managers’ Index (PMI). Regarded as the leading indicators of economic growth, both manufacturing and services PMI indicate the likelihood of upward expansion.

Earlier in the week, the release of the November data from the U.S. labor market indicated that it is poised for a rebound. The number of job openings in October climbed to 7.74 million, up from September’s revised 7.37 million reading. While layoffs during the month hardly changed, the number of Americans quitting jobs voluntarily (regarded by some as a better measure of labor market conditions) increased to 3.3 million. New jobs added, expected to be 220,000, overshot consensus and registered 227,000, and the weaker data reported for last month was revised higher. The unemployment rate broadly ticked higher to 4.2%. However, this remains well below the long-term averages of around a 5.7% unemployment rate in the U.S.

Metals and Mining

Gold and silver remain confined in a consolidation pattern as investors anticipate a new catalyst for a breakout. Investors traverse a balancing act between rising inflation risks, geopolitical uncertainties, and a shallower easing cycle that tends to strengthen the U.S. dollar and higher bond yields. Although the current price fluctuations of these precious metals tend to disappoint ahead of the coming new year, analysts nevertheless remain bullish. While it may take time for the markets to adjust to the new administration that formally takes over on January 20, 2025, financial institutions such as Goldman Sachs, Bank of America, the CIBC, and other Canadian banks see gold prices likely to push to $3,000 per ounce next year. Towards the second half of 2025, gold prices may rally as the threat of a global trade war drives inflation higher and dampens economic growth.

The spot prices of precious metals ended mixed for the week. Gold ended at $2,633.37 per troy ounce, lower by 0.37% from last week’s close at $2,643.15. Silver came from $30.63 last week to close this week at $30.97 per ounce for a 1.11% gain. Platinum fell by 1.93% from its close last week at $949.90 to settle this week at $931.55 per troy ounce. Palladium closed this week at $960.29 per troy ounce, 2.32% lower than its close last week at $983.09. The three-month LME prices of industrial metals were mostly up for the week. Copper closed this week higher by 0.71% from its previous weekly close at $9,010.50 to end the week at $9,074.50 per metric ton. Aluminum climbed by 1.73% from its previous close at $2,594.00 to end the week at $2,639.00 per metric ton. Zinc ascended by 0.50% from its previous weekly close at $3,103.00 to close this week at $3,118.50 per metric ton. Tin gained 0.87% from last week’s close at $28,913.00 to end this week at $29,165.00 per metric ton.

Energy and Oil

OPEC+ postponed its scheduled supply increases by another quarter, as widely anticipated. It is now promising to start unwinding output cuts beginning April 2025 and beyond. This reset simultaneously extends the full unwinding of output cuts by a year until the end of 2026 as the oil group addresses rising non-OPEC production. This pronouncement failed to convince the oil markets that the bulls would take over in the foreseeable future. Even the postponement of the UAE’s baseline quota increase could not stop ICE Brent from slipping back below $72 per barrel.

Natural Gas

For the report week beginning Wednesday, November 27, to Wednesday, December 4, 2025, the Henry Hub spot price fell by $0.52 from $3.35 per million British thermal units (MMBtu) to $2.83/MMBtu. Regarding Henry Hub futures prices, the December 2024 contract expired on Tuesday, November 26, at $3.431/MMBtu. The price of the January 2025 NYMEX contract decreased by $0.16, from $3.204/MMBtu at the start of the report week to $3.043/MMBtu by the week’s end. The price of the 12-month strip averaging January 2025 through December 2025 futures contracts declined by $0,08 to $3.161/MMBtu. At most locations this report week, natural gas spot prices fell. Price changes ranged from a decrease of $0.52 at the Henry Hub to an increase of $0.68 at Northwest Sumas.

International natural gas futures prices increased during the report week. The weekly average front-line futures prices for liquefied natural gas (LNG) cargoes in East Asia increased by $0.09 to a weekly average of $15.06/MMBtu. Natural gas futures for delivery at the Title Transfer Facility (TTF) in the Netherlands increased by $0.24 to a weekly average of $14.82/MMBtu. In the week last year corresponding to this report week (beginning November 29 and ending December 6, 2023), the prices were $16.10/MMBtu in East Asia and $12.91/MMBtu at the TTF.

World Markets

As jitters about political instability in France abated, the pan-European STOXX Europe 600 Index closed 2.00% higher in local currency terms. Faster policy easing by the European Central Bank (ECB) appeared to be anticipated by the markets. The major European stock indexes likewise climbed. France’s CAC 40 Index added 2.65%, Germany’s DAX rose by 3.86%, and Italy’s FTSE MIB ascended by 4.00%. The UK’s FTSE 100 Index gained by 0.26%. The political concerns in France arose when Prime Minister Michel Barnier’s minority government collapsed after a no-confidence motion was backed by Parliament. The motion was tabled by the National Rally (NR) and left-wing New Popular Front to block the proposed deficit-reducing budget for 2025.

The Week Ahead

In the coming week, watch out for important economic releases such as the CPI and PPI inflation data, wholesale inventories for October, and revised U.S. productivity data for the third quarter. The effect was for the yield spread between German 10-year bunds and French 10-year OATS – a metric for political and financial risk in the Eurozone – to widen at one point to 90 basis points, the most since 2012. Subsequently, the gap narrowed to below 80 basis points after President Emmanuel Macron said he would appoint a new prime minister in “coming days.” He also promised to meet with political leaders from both sides of the aisle to form a new “government of general interest.” On the economic front, the key macroeconomic data in Europe continued to signal a slowing economy in the fourth quarter of 2024. Mainly due to drops in sales of non-food products and auto fuel, Eurozone retail trade volumes decline in October by 0.5% sequentially, after increasing by 0.5% in September. Manufacturing continued to struggle in Germany. Industrial output fell by 1.0% month-over-month, which falls short of expectations for a 1.2% rebound. A decline in the demand for machinery and equipment led to a slump in factory orders by 1.5% for the month.

Japan’s equities rose during the week. The Nikkei 225 Index gained 2.3% while the broader TOPIX Index added 1.7%. The rosy profit outlooks for Japan’s export-heavy industries are supported by the weakness of the nation’s currency. The yen depreciated to approximately the middle of the JPY 150 range against the greenback, from the high JPY 149 range at the end of the previous week. Regarding fixed income, due to the persistent uncertainty about the Bank of Japan’s (BoJ’s) rate hike plans, the yield on the 10-year Japanese government bond closed the week broadly flat at 1.06% after trading in a narrow range. According to Toyoaki Nakamura, a member of the BoJ’s board, a judgment on the merits of incoming data will determine any forthcoming interest rate hike, particularly regarding wage and economic growth. The timing of the next 25-basis-point rate hike is deemed by investors to be split between December and January. The likelihood of a January rate hike is suggested by a recent commentary by BoJ Governor Kazuo Ueda on the need to observe 2025 wage trends and whether wage hikes are being reflected in service prices. Uncertainty around U.S. economic policy remains to be clarified, particularly on the future imposition of tariffs. Average nominal wages grew by 2.6% year-on-year in October, up from a revised 2.5% in September and matching consensus expectations. Real wage growth (adjusted for inflation) remained unchanged following a 0.4% contraction. Household spending fell by 1.3% year-on-year, a reduction for the third consecutive month.

China stocks saw gains in the past week as investors anticipate fresh stimulus measures. Resilient manufacturing data released during the week also supported equities performance. The Shanghai Composite Index climbed by 2.33%. Likewise, the blue-chip CSI 300 was up by 1.44%. The Hong Kong benchmark Hang Seng Index added 2.28%. During the Central Economic Work Conference, an annual meeting where top officials map out the economic agenda for the next year, analysts expect China’s leadership to announce further action to support the economy. Among the topics investors look forward to are economic growth targets and plans for more stimulus. The meeting will last for two days, beginning December 11. There are high expectations that Beijing will roll out additional measures to address growth risks that may be posed by the trade policies of the incoming Trump administration. Economic news released showed that China’s factory activity expanded for the second consecutive month. According to the statistics bureau, the official manufacturing Purchasing Managers’ Index (PMI) increased to a higher-than-expected 50.3 in November from 50.1 in October. The measure of construction and services activity, the nonmanufacturing PMI, fell to a below-consensus 50 in November from 50.2 in October. The 50-mark delineates expansion and contraction.

Key Topics to Watch

- Wholesale inventories for Oct.

- NFIB optimism index for Nov.

- U.S. productivity (revision) for Q3

- Consumer price index for Nov.

- CPI year over year

- Core CPI for Nov.

- Core CPI year over year

- Monthly U.S. federal budget

- Initial jobless claims for Dec. 7

- Producer price index for Nov.

- Core PPI for Nov.

- PPI year over year

- Core PPI year over year

- Import price index for Nov.

- Import price index minus fuel for Nov.

Markets Index Wrap-Up