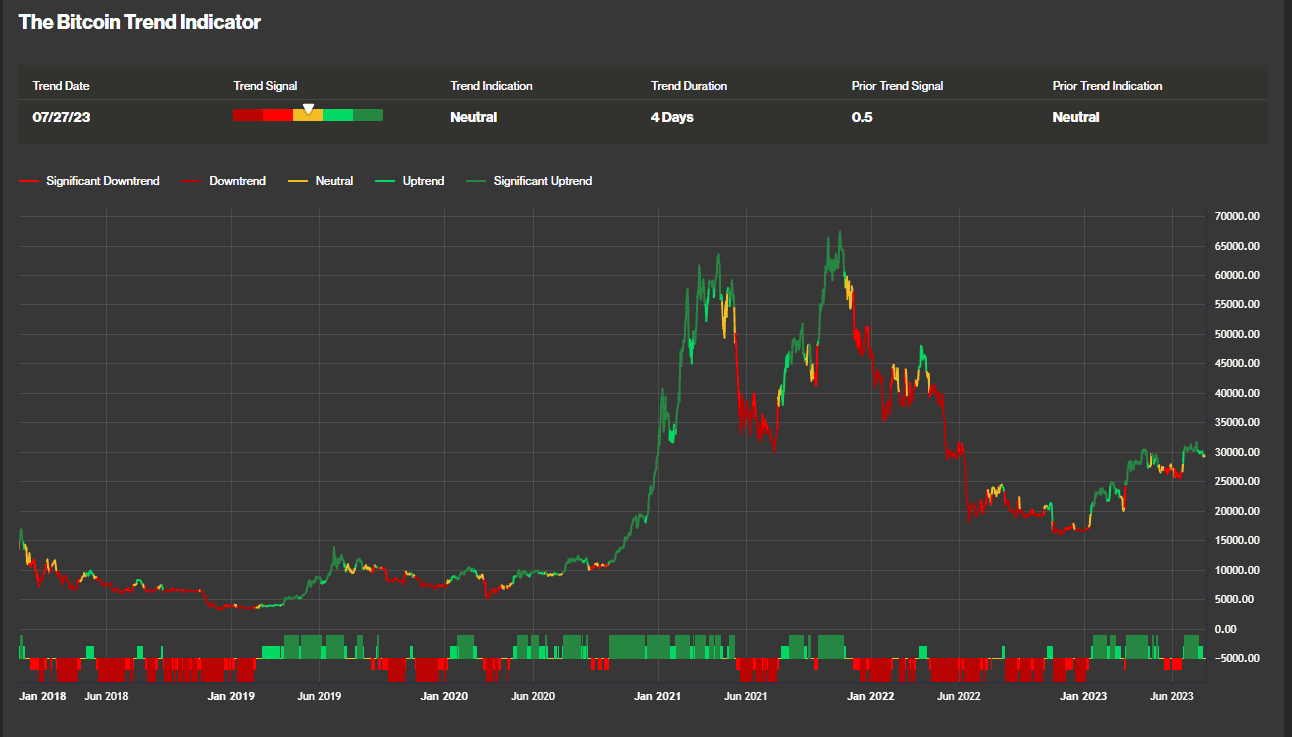

With just three days remaining in July, bitcoin (BTC) and ether (ETH) are poised to finish in negative territory for the month. Over the most recent seven days, bitcoin and ether fell -1.59% and -0.81%, respectively, very much in line with what has been a range-bound trading environment for the entire month.

Both of the cryptos have moved into neutral territory per their respective CoinDesk Indices trend indicators. The gauges, calculated daily, are designed to illustrate price direction and momentum strength using a series of moving averages.

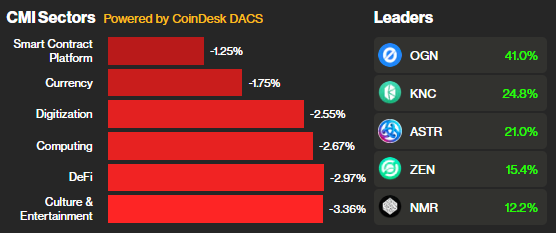

Broader moves across the entire digital asset landscape are captured within the Coindesk Market Indices (CMI), and all CMI sectors finished in the red this week, including the DeFi Index (DCF), down 1.24%. The weakest performer was the Culture and Entertainment Index (CNE), off 3.24%.

The monthly picture is marginally more promising, with all CMI sectors finishing in the green, with the exception of the Currency Index (CCY), down 0.39% in July, in part thanks to bitcoin’s sizable weighting in that grouping.

Of the 183 assets within CMI, 112, or 61% have outperformed bitcoin in July.

Weekly movers

NFT platform Origin Protocol (OGN) rose 32% over the past week, while DeFi’s Kyber Network (KNC) and smart contract platform Astar (ASTR) added 23% and 22%, respectively.

With each of these tokens boasting market caps below $300 million, they are apt to fall underneath the radar. Still their sector alignment can provide insight into whether their performance was in line with similar assets.

OGN’s gain this week stands in contrast to the Culture and Entertainment Index (CNE), which was lower by 3.1%. KNC’s advance came alongside a 2.8% decline for the DeFi Index (DCF), and ASTR’s rise outperformed the 1.2% fall for the Smart Contract Platform Index (SMT).

Looking ahead to next week

On the heels of this week’s Federal Reserve interest rate increase and inflation data, next week’s macroeconomic focus will center on jobs, in particular Friday’s Nonfarm Payrolls report for July. Less followed, but also of interest will be Tuesday’s Job Openings and Labor Market Survey (JOLTS).