The U.S. economy is closely related to the U.S. stock market. But that relationship is not perfect in a number of ways.

An important way the two differ is international exposure.

According to FactSet, S&P 500 companies1 generate around 40% of revenue outside of the U.S.2 That means these companies are significantly dependent on the health of the international economies in which they operate. They employ abroad, source goods abroad, and sell abroad.

This is not to say the U.S. economy is totally decoupled from the rest of the world: Annual exports account for $3 trillion of the $25 trillion worth of U.S. GDP.

But when you think of the U.S. economy, you generally think about activity inside the borders of the U.S. This includes U.S. employment levels, U.S. manufacturing activity, U.S. services sector activity, etc. This, by the way, includes non-U.S. companies with footprints in the U.S. like Toyota, B.P., Samsung, and Nestle.

We’re discussing this now because of news from FedEx FDX -1.25%↓ , a U.S.-based S&P 500 company. From the company’s press release on Thursday (emphasis added):

First quarter results were adversely impacted by global volume softness that accelerated in the final weeks of the quarter. FedEx Express results were particularly impacted by macroeconomic weakness in Asia and service challenges in Europe, leading to a revenue shortfall in this segment of approximately $500 million relative to company forecasts. FedEx Ground revenue was approximately $300 million below company forecasts.

FedEx is one of the so-called “early reporters” — that is, companies whose quarters end a month earlier than most companies. The last two months of FedEx’s quarter overlaps with the first two months of most companies’ Q3. And so the company’s warning may serve as a leading indicator for the upcoming Q3 earnings season, which kicks off in mid-October.

As Asia struggles with COVID-related lockdowns and Europe wrestles with surging energy costs, companies with significant exposures in these regions may underperform those with greater dependence on the U.S., where the economy has been resilient.

There’s also the matter of the surging U.S. dollar, which is leading to the dollar value of revenue generated abroad shrinking for U.S.-based multinational companies. Morgan Stanley analysts recently estimated that every 1% increase in the dollar index represents a roughly 0.5% reduction in S&P 500 earnings per share.

While dollar strength may be good news for U.S. importers and American vacationers traveling abroad, it’s bad news for everyone else watching their own currencies lose purchasing power in the international markets.

All of this raises doubt about analysts’ current forecasts for earnings growth, which appear at risk of getting revised down further. This is a big deal because, as TKer readers know, earnings are the most important driver of stock prices over the long run.

For investors and traders, the key question is what’s priced into the markets. The strong dollar and economic weakness abroad are known stories that have weighed on markets for a while. So, while these are clear headwinds, it’s very possible to see markets climb as analysts factor in the deteriorating macro backdrop into their earnings forecasts.

Reviewing the macro crosscurrents 🔀

There were a few notable datapoints from last week to consider:

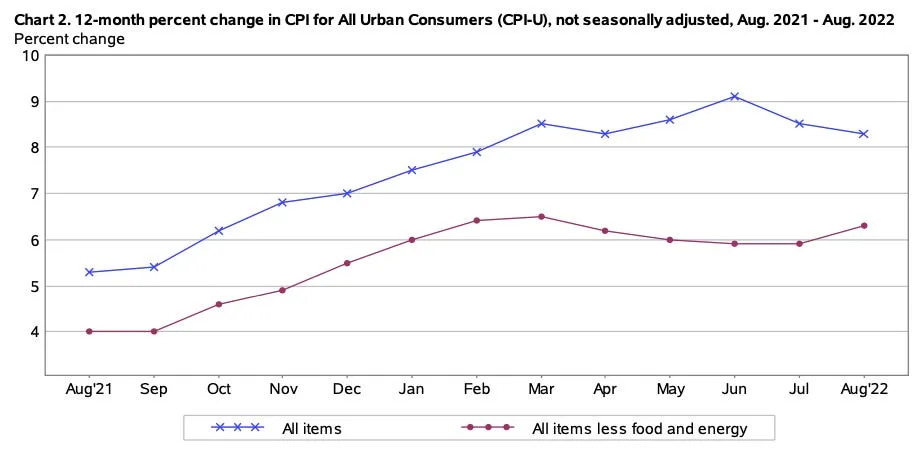

- 🎈 Inflation is still high. The consumer price index climbed 0.1% month over month in August, unexpectedly accelerating from 0.0% in July. Economists had expected the metric to decline 0.1% amid falling energy prices. While energy prices indeed fell during the period (gasoline prices tumbled 10.6%), prices for food and shelter remained hot, rising 0.8% and 0.7%, respectively. Excluding food and energy prices — which tend to be more volatile in the short run — core CPI growth unexpectedly accelerated to 0.6% in August from 0.3% in July. On a year-over-year basis, CPI was up 8.3% (hotter than expected), and core CPI was up 6.3% (also hotter than expected).

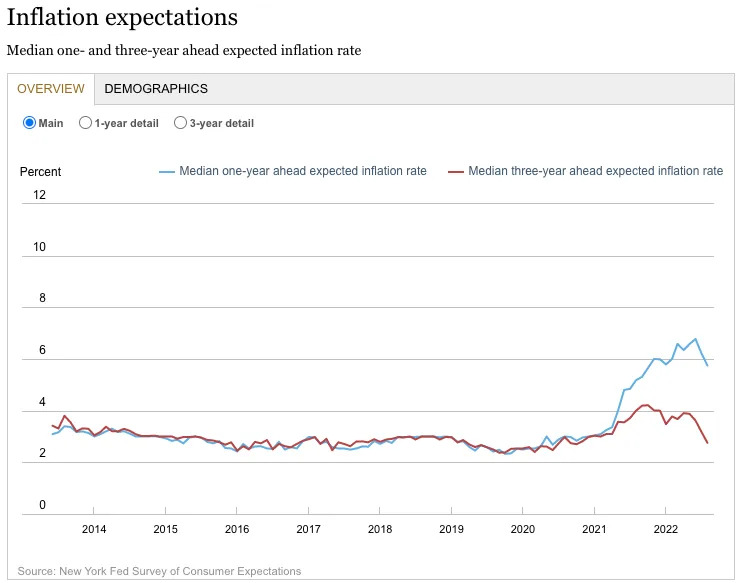

- 📉 Expectations for inflation are coming down. From the University of Michigan’s September Survey of Consumers: “With continued declines in energy prices, the median expected year-ahead inflation rate declined to 4.6%, the lowest reading since last September. At 2.8%, median long run inflation expectations fell below the 2.9-3.1% range for the first time since July 2021.“ The New York Fed’s August Survey of Consumer Expectations released Monday echoed this sentiment. The median expectation for inflation one year ahead was 5.7% in August, down from its June high of 6.8%. From the NY Fed: “Expectations about year-ahead price increases for gas also continued to decline, with households now expecting gas prices to be roughly unchanged a year from now.“

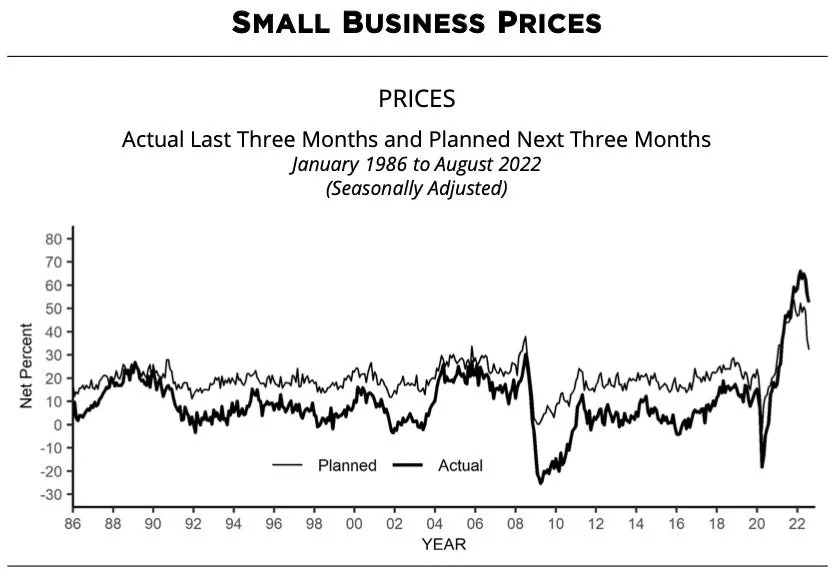

- 🏪 Small businesses are cooling on prices. From the NFIB: “The net percent of owners raising average selling prices decreased 3 points from July to a net 53% seasonally adjusted.“

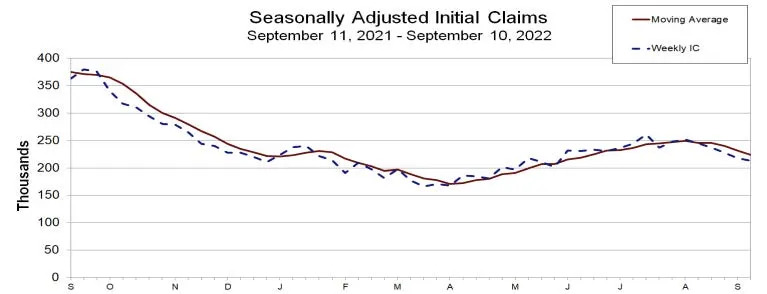

- 💼 The labor market is strong. Even as the economy cools and hiring slows, employers seem to be holding on tight to their employees. Initial claims for unemployment insurance came in at 213,000 for the week ending September 10, down from 218,000 the week prior. While the number is up from its six-decade low of 166,000 in March, it remains near levels seen during periods of economic expansion.

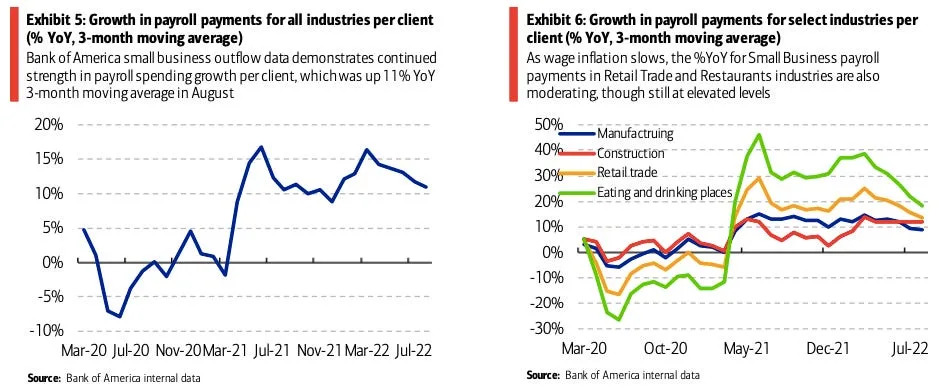

- 💵 Small businesses are hiring. From Bank of America: “…small businesses continue to see strength in payroll payments. The three-month rolling average of payroll spend per client rose 11% year-over-year (YoY) in August, suggesting robust hiring and wage growth momentum. Restaurant and bar payroll payments may be moderating the most from recent highs, partly reflecting easing wage inflation in leisure & hospitality, but even here 18% YoY growth in August is reassuring.”

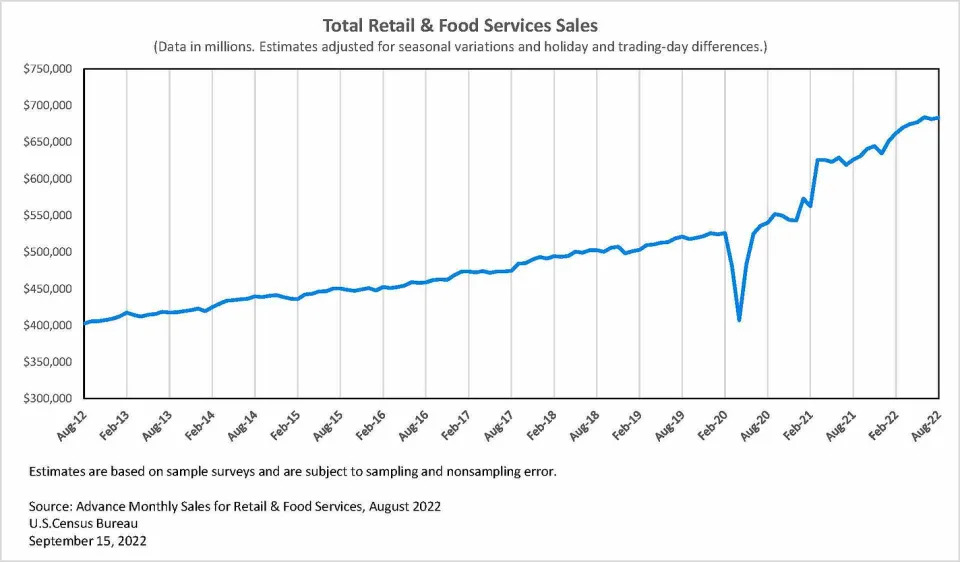

- 🛍 Retail sales are holding up. In August, retail sales unexpectedly climbed by 0.3% month over month. Autos sales climbed 2.8% while gas station sales fell 4.2%. Excluding autos and gas, sales increased by 0.3%, which wasn’t as strong as the 0.5% gain expected. The report reflected strength in “doing stuff” — restaurant and bar sales were up 1.1% — and weakness in “buying stuff” — furniture sales were down 1.3%. Note: Retail sales figures are not adjusted for inflation. Real sales levels are lower.

- ⛓ Supply shortages are less of a problem. Business inventories increased by 0.6% month-over-month in July. This brought the inventory/sales ratio to 1.32.

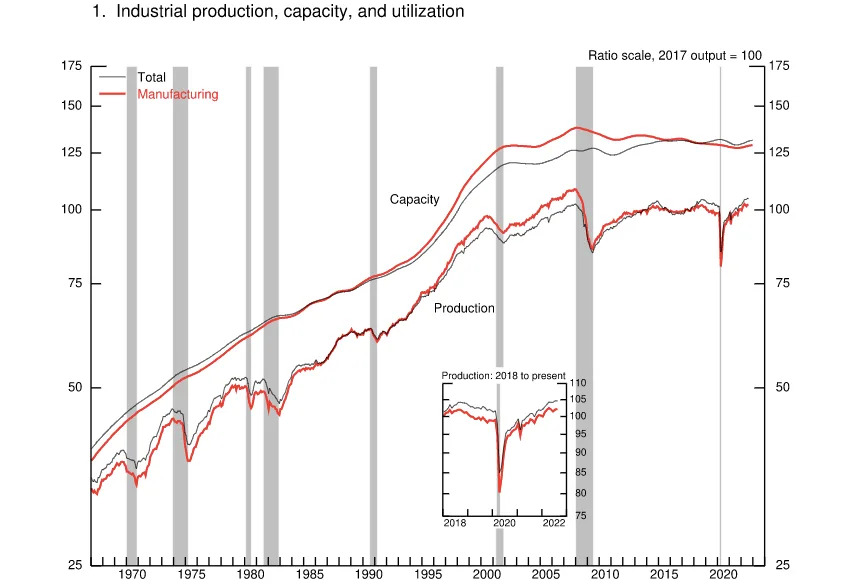

- 🛠 Manufacturing cools. Industrial production activity declined by 0.2% month over month in August.

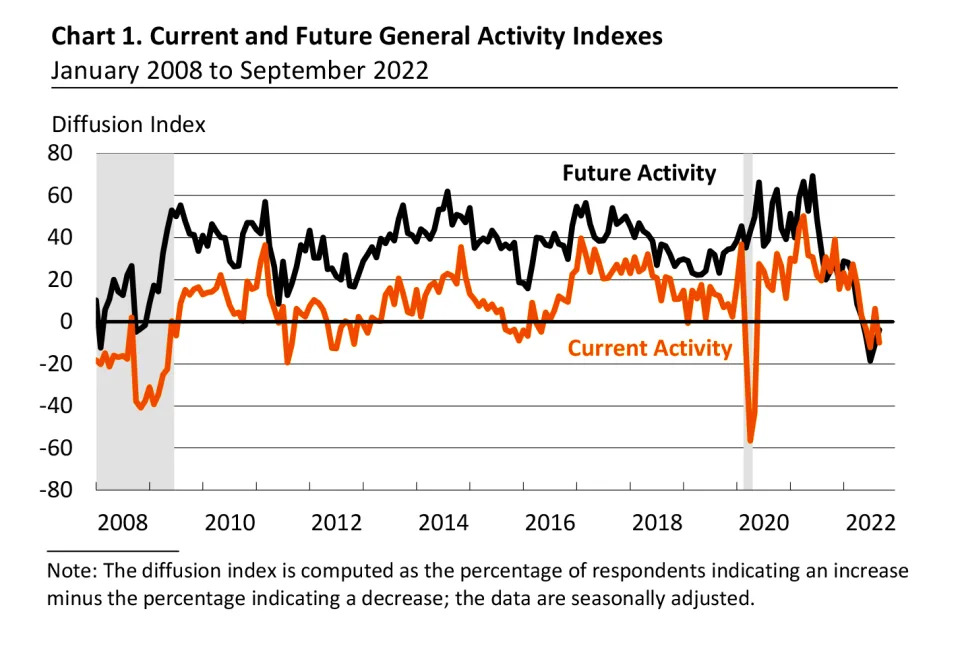

- 🥶 Manufacturing looks to keep cooling. The Empire State Manufacturing Survey’s general business conditions index and the Philly Fed Manufacturing Business Outlook Survey’s current activity index both registered negative prints in September, suggesting manufacturing activity in the Mideast U.S. continued to contract.

undefined

- 📉 Stocks tumbled last week with the S&P 500 falling 4.7% to close at 3,873.33. The index is now down 19.2% from its January 3 closing high of 4,796.56 and up 5.6% from its June 16 closing low of 3,666.77.

Putting it all together 🤔

Retail sales and manufacturing activity data confirm that the economy continues to cool. Meanwhile, inventory levels continue to rise, suggesting supply chains constraints continue to ease.

The strong labor market — marked by low layoff activity — continues to put money in consumers’ pockets, preventing the bottom from falling out of consumer spending. Unfortunately, the strong consumer is part of the reason why inflation has been high.

Indeed, while some price indicators have been easing, inflation remains troublingly high. And so financial markets remain volatile as the Fed increasingly tightens financial conditions in its effort to cool prices. As such, recession risks linger and analysts have been trimming their forecasts for earnings. For now, all of this makes for a conundrum for the stock market until we get “compelling evidence” that inflation is indeed under control.