Never have Americans saved so much money and earned so little on it.

For those stashing cash, the average savings account rate is down to just 0.05%, or even less, at some of the largest retail banks, according to the Federal Deposit Insurance Corp.

Rates have fallen significantly since the Federal Reserve cut its benchmark rate to essentially zero to combat the economic effects of the coronavirus crisis. (Although the Fed has no direct influence on deposit rates, they tend to be correlated to changes in the target federal funds rate.)

At the same time, bank deposits have ballooned since the start of the Covid-19 outbreak, pushing rates even lower and allowing banks to reduce what they pay depositors.

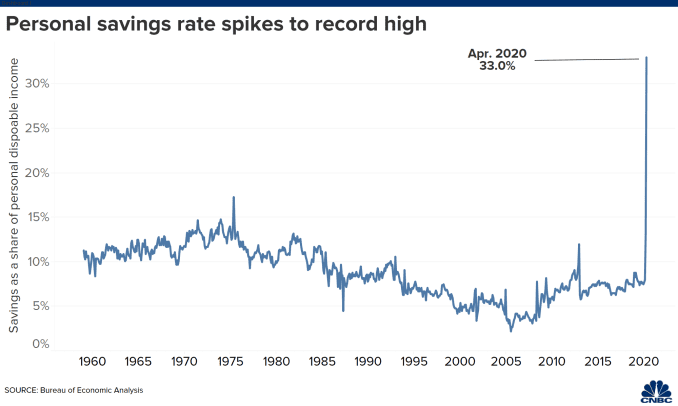

With so many Americans at a standstill, the personal savings rate — how much people save as a percentage of their disposable income — hit a historic 33% in April.

It has since backed off that record high as pandemic-related assistance programs started to wind down. However, the rate is still near 13%, according to the latest data from the U.S. Bureau of Economic Analysis, higher than it has been in four decades.

“Even at rock-bottom interest rates, banks have been inundated with deposits just as loan demand dropped off,” said Greg McBride, chief financial analyst at Bankrate.com.

As long as the economy continues to struggle, the Fed has said it will keep rates down. That means savers shouldn’t hold out much hope for a better deal in the year ahead, according to McBride.

“If loan demand starts to accelerate, that could be a catalyst for some higher rates, but we have to get there first,” he said.

Alternatives for stashing your cash

Historically, an old-fashioned certificate of deposit was a decent way to lock in a slightly better return.

Currently, one-year CD rates are averaging just under 0.5%, which means savers are locking in funds below the rate of inflation and getting nearly nothing in return.

The CDs that offer the highest yields typically have higher minimum deposit requirements and require longer periods to maturity. Right now those yields are no better.

“CD yields are at record lows across the maturity spectrum,” McBride said. “There’s very little advantage in longer maturities.”

Online-only banks such as Marcus by Goldman Sachs and CIT Bank offer slightly higher returns, thanks in part to lower overhead expenses than traditional banks. However, even the most competitive banks are steadily lowering their rates, as well.

Just one year ago, high-yield savings accounts were offering as much as 1.75%. Now, the average online savings account yield is 0.51%, down from 0.54% in December.

“We’ve never seen this kind of decline,” said Ken Tumin, founder of DepositAccounts.com.

In the last month, they notched their smallest decrease since the start of the pandemic, which suggests “we might be near a bottom,” Tumin added.

For now, a better bet could be high-yield reward checking accounts, Tumin advised, which are offered at some regional banks and credit unions.

“The rates are falling there, too, but not as much as online savings accounts.”

The current average yield on these accounts is 1.54%, although not all customers will qualify.

Unlike regular checking accounts, which often impose minimum-balance requirements, high-yield accounts have maximum balance limits of $10,000 to $20,000, depending on the bank, and could also require a minimum number of monthly debit card transactions among other conditions.