There’s little question that Social Security is our nation’s most important social program. According to an April-released survey from national pollster Gallup, 89% of current retirees rely on their monthly payout to some degree to help make ends meet. Meanwhile, an all-time record 88% of nonretirees told Gallup that they expect to lean on Social Security as either a major or minor source of income during retirement.

Furthermore, an analysis from the Center on Budget and Policy Priorities in 2016 found that elderly poverty levels are less than 9% with Social Security, but would be north of 40% if the program didn’t exist.

Suffice it to say, Social Security benefits often play a key role in the financial well-being of our nation’s retired workforce. This means there’s arguably no decision more important for seniors than deciding when to begin taking their payout.

How are Social Security benefits calculated?

In total, there are more than a half-dozen factors that can affect how much a person is paid monthly from Social Security, or how much of that payout they’ll be allowed to keep. But of these more than half-dozen factors, four stand head and shoulders above the rest.

The first two are inextricably linked: work history and earnings history. When the Social Security Administration (SSA) calculates a workers’ monthly retirement benefit, they do so by taking into account their 35 highest-earning, inflation-adjusted years. For each year less of 35 worked, the SSA averages in $0, which will reduce the amount a worker is paid on a monthly basis.

The third factor that influences what’s paid monthly by Social Security is a person’s birth year, which determines a person’s full retirement age — i.e., the age at which a beneficiary can receive 100% of their monthly payout. Put simply, taking benefits prior to reaching full retirement age means accepting a permanent reduction to your monthly payout. Conversely, claiming your benefit after your full retirement age can permanently increase your monthly payout.

The fourth and final factor is claiming age. Social Security retirement benefits can begin at age 62, or any time thereafter. The catch is that monthly benefits increase by up to 8% annually, through age 69, every year an eligible retiree holds off on taking their payout.

The most important Social Security table you’ll ever see

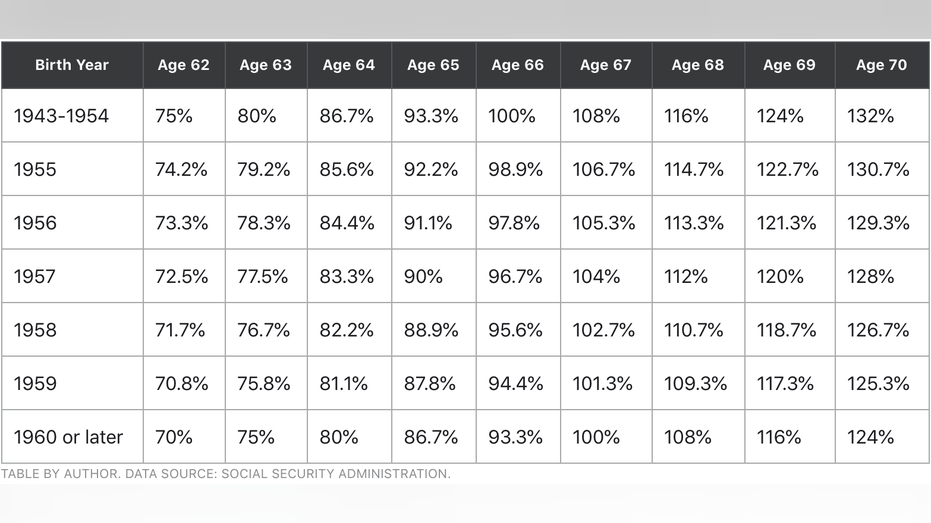

Claiming age can absolutely have the biggest impact on what you’ll receive on a monthly or lifetime basis from the Social Security program. But in order to make the smartest possible claiming decision, future beneficiaries must understand how their full retirement age and claiming age can help or hinder their Social Security income-earning capacity. That’s why the following table is a must-see for all future retirees.

As you can see, Social Security’s full retirement age doesn’t change a lot. People born prior to 1955 have a full retirement age of 66, while those born in 1960 or later will have a full retirement age of 67. For baby boomers born between 1955 and 1959, the full retirement age increases by two months each year.

In order to understand how your full retirement age and claiming decision can impact what you’ll receive monthly, we first need to begin with a baseline figure. In Aug. 2020, the SSA listed the average retired worker benefit at $1,517.44 a month, which is what we’ll use in our example.

For baby boomers born on the early side (i.e., between 1946 and 1954), the table is pretty clear. If you take benefits prior to age 66, you’re facing a reduced monthly payout of up to 25%. Likewise, waiting until age 70 can increase what you’ll receive monthly by up to 32%. Thus, a claim at age 70 for an early boomer could net $2,003.02 a month, using our baseline figure of $1,517.44.

Things change a bit for those born between 1955 and 1959. Let’s say you’re born in 1958, which makes 2020 your first year of eligibility to claim benefits. Should you choose to take your payout at age 66, you’ll only net 95.6% of your full payout ($1,450.67).

For very late boomers, Gen X, millennials, and Generation Z, you’ll need to wait even longer to receive a bigger payout. Claiming at age 62 could mean accepting an up to 30% permanent reduction ($1,062.21), although waiting until age 70 only provides a 24% bump-up in monthly benefits ($1,881.63), down from 32% for those born between 1943 and 1954.

But wait — there’s more

While it’s incredibly important to understand how your full retirement age and claiming decision affect what you’ll receive on a monthly basis, another figure should take precedence: your lifetime benefits.

It ultimately doesn’t matter how much you’re paid by Social Security each month, as long as you’re maximizing what you’ll receive from the program over your lifetime. Admittedly, there’s no concrete way to know if you’ve made the optimal claiming decision because we (thankfully) don’t know our expiration date ahead of time. We can, however, use certain clues and variables to our advantage when making a claiming decision.

As an example, a person in poor health who has one or more chronic conditions might be best off taking their payout early. Yes, this would mean a reduced monthly payout, but it would also likely result in this individual netting the greatest lifetime benefit from the program.

Another consideration here is marital status. A substantially higher-earning individual who takes their payout before reaching full retirement age will reduce the monthly benefit available to their surviving spouse. Thus, waiting to claim benefits as a higher-earning spouse can ensure that their significant other is financially protected in the event of an untimely passing.

Knowing your monthly payment is important, but netting the maximum possible lifetime benefit is paramount.