Huge sums of investor cash have poured into exchange-traded funds during this past year (and during the whole bull market) with billions of dollars sitting passively in funds betting on the very largest U.S. stocks.

But new research suggests this money is betting on funds with a methodology that might not offer the best returns for the regular person over the long term.

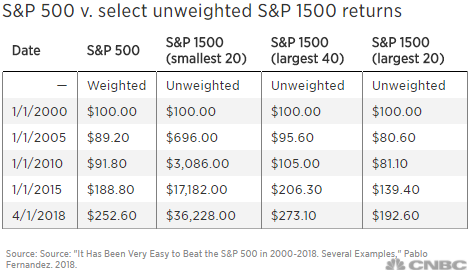

The weighting of stocks in most major indexes, and the ETFs tied to them, are based on market capitalization, meaning that big-company components can pull the index more than the little ones. For example, a 20 percent move in Apple can shift the entire S&P 500 by more than half a percent.

An equal-weighted index, on the other hand, treats all the companies equally in terms of how they can influence the group as a whole and in many cases, offered a better return to investors over the last 20 years, according to Pablo Fernandez, a finance professor at the University of Navarra in Spain.

For example, researchers there showed that if an investor had put $100 in the S&P 500 in January 2000, the sum would be worth $252.60 in April 2018; alternatively, $2.50 invested unweighted in the largest 40 companies in the S&P 1500 would be worth $273.10 in April 2018.

Investors have poured more than $17 billion into that ETF over the past year, according to FactSet fund flow data; Vanguard’s S&P 500 fund drew nearly $12 billion over the same time.

“We document that unweighted indexes have outperformed weighted indexes and that the S&P 400 and the S&P 600 have outperformed the S&P 500,” the University of Navarra researchers wrote. The S&P 400 tracks midcaps while the S&P 600 tracks small caps.

The debate

Chris Brightman of Research Affiliates says a simple equal-weighted strategy can do even better when combined with regular rebalancing.

Rebalancing is essentially trimming stocks that have outperformed and buying those that have underperformed given a historical tendency for prices to revert to an average. In essence, Brightman added, it’s betting against the current Wall Street momentum darlings in favor of stocks that have underwhelmed or scared investors.

“One can turn that mean reversion into profits by rebalancing their portfolio by selling securities that have outperformed and buying securities that have underperformed,” he added.

That strategy, the CIO said, provided about a 2-percent premium over the market over several decades.

His firm, founded by Rob Arnott, has long advocated for weighting stocks by fundamental measures to garner better passive returns than the industry norm.

“We use the fundamental index, which targets an invest amount for each company which is proportional to its fundamental size. Things like size, cash flow and dividends,” said Brightman.

.1531240391711.jpeg)

To be sure, though, equal weighed indexes don’t always outperform their market weighted cousins, especially during prolonged outperformance or underperformance in isolated areas of the market. Should a select few firms (or a sector) consistently outperform, for example, each time an investor rebalances their portfolio back to equal, they could be missing out on future gains in those areas.

“You would have done terribly with your equal-weighted strategy during the 1990s, during the dotcom bubble,” Brightman said. “If you decided to present this to a board or a committee in 1995, by 1997 or 1998 you’d think you were really stupid. However, you would have dramatically outperformed the market in 2000, 2001, 2002 and 2003.”

The Invesco S&P 500 Equal Weight ETF, which replicates the performance of the equal-weighed S&P 500 index has returned 4.2 percent so far this year against the S&P 500’s 5.8 percent return. Much of that disparity is likely due to the prolonged outperformance in the larger technology stocks, which have a bigger weighting in the S&P 500.

But over the last ten years, the equal weight ETF has returned 11.8 percent annually, more than the 10.8 percent return from the S&P 500.